The European Securities and Markets Authority introduced the European Single Electronic Format (ESEF) mandate to improve the way financial disclosures are made by listed companies in the EU and used by various stakeholders such as national regulators and investors.

The Inline XBRL or iXBRL format, in which the companies need to prepare their annual reports, makes corporate disclosures comparable across companies and sectors, while also improving their accessibility and quality.

The question to ask then is if the ESEF iXBRL mandate has made a difference to the quality of reporting by the companies it governs.

Team Fin-X Solutions conducted a study of the 2020 ESEF iXBRL annual reports of 447 companies in the EU and the UK. The study yielded several useful insights, which we will discuss below.

Scope and methodology of the Fin-X Solutions Study

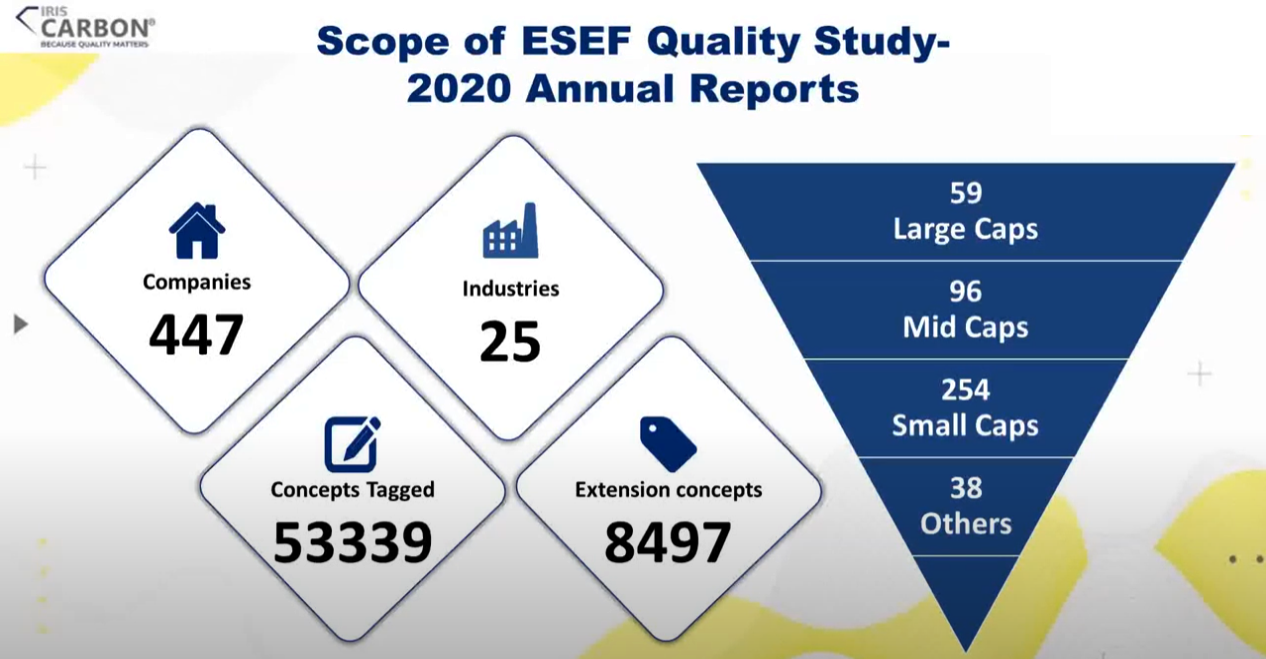

The following image will give you a snapshot of the Fin-X Solutions study.

Source: Fin-X Solutions internal study

Source: Fin-X Solutions internal study

We studied the ESEF iXBRL filings of 447 companies across 13 EU countries and the UK (14 countries in all). The companies belonged to 25 different industries. Over half of them were small caps, 21% were mid-caps, and 13% were large caps.

As many as 225 companies belonged to countries in which filing the 2020 annual reports in iXBRL was mandatory — Austria, the Czech Republic, Germany, and Slovenia — while 222 companies had filed in iXBRL voluntarily.

Our research methodology involved downloading the zip packages constituting each company’s iXBRL submission from the respective country’s Officially Appointed Mechanism and running each filing through our in-house validator IRIS Bushchat®. Two types of validation results were recorded.

We found over 50,000 tagged concepts in the 447 companies’ filings and a little over 8,000 extensions.

A note about tagging and extensions: Tagging involves mapping the disclosures in an annual report to the corresponding concepts in the ESEF taxonomy. Extensions or extension elements are custom tags formed to represent disclosures for which the right-fit concept cannot be found in the ESEF taxonomy. The correct practice is to study the ESEF taxonomy and identify the concepts that pertain to your disclosures. Extensions should be used only when necessary for ESEF reports to be of high quality.

Validation errors and warnings

Our validation checks revealed that only 176 of the filings we studied were totally error-free. The remaining filings threw up 3204 errors and 11609 warnings in all.

What are errors and warnings?

An error is defined as an issue in an ESEF filing that needs immediate attention. A filing with errors risks being rejected by the OAM if the errors are not rectified. An example of this is a faulty ESEF iXBRL zip package which is not in compliance with the ESEF reporting manual.

A warning is less severe than an error and does not impede submission through the OAM as it may still be considered a valid ESEF filing. Warnings need to be checked and corrected, nonetheless. Rounding errors are an example of this type of issue.

Note: Our analysis was based on the tagging of the 5 primary financial statements by the companies using the ESEF iXBRL standard. Subsequent phases of this mandate will require companies to tag notes and other detailed information which may increase the percentage of errors and warnings in subsequent filings.

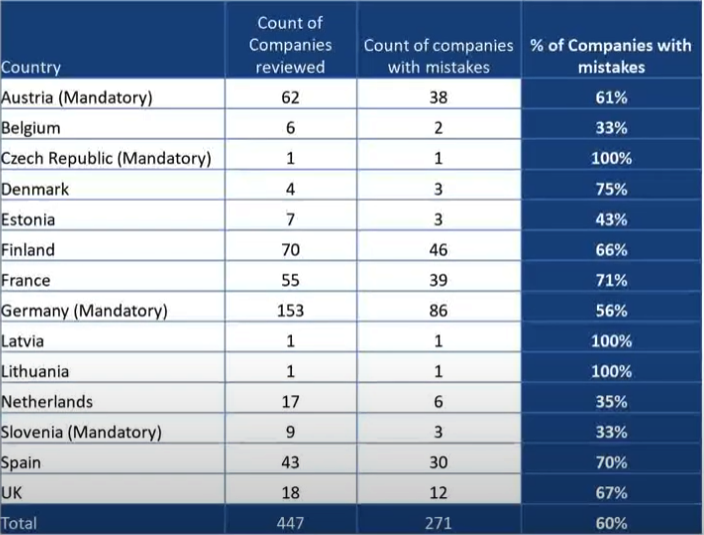

ESEF filing errors — Country-wise distribution

A few observations from the country-wise distribution of ESEF errors:

Over a third of the companies whose filings Fin-X Solutions surveyed were from Germany.

Among countries with at least 5 ESEF participants, France was found to have the highest proportion of companies with mistakes in their ESEF filings (71%).

Belgium and Slovenia had the lowest proportion of companies with mistakes in their ESEF filings (33%).

Table 1: Country-wise Distribution of ESEF iXBRL filings

Table 1: Country-wise Distribution of ESEF iXBRL filings

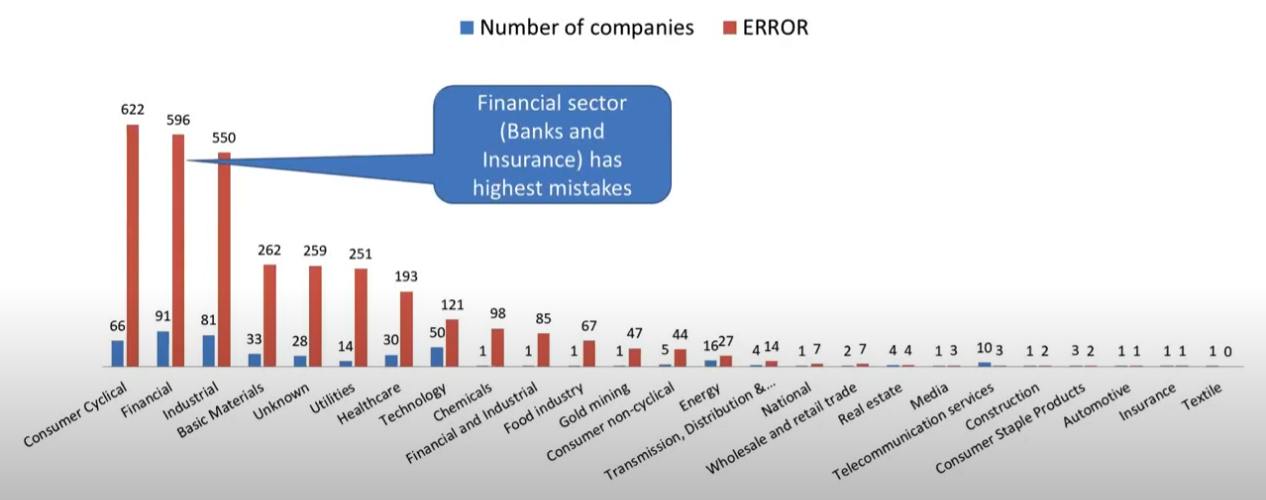

ESEF filing errors — Industry-wise distribution

A total of 25 sectors were part of our study and the table below illustrates how many companies from each sector were studied along with the total number of errors that were found in their AFRs.

A surprising finding from the study saw the Financial (BFSI) sector come out with the most errors in their ESEF iXBRL filings, followed by the Consumer Cyclical sector in a close second. This may call for special attention as the concepts provided by the ESMA reference taxonomy may not be fully in line with current reporting practices and there may be a need to create custom elements or extensions.

We will now take a brief look at the industry-wise breakdown of the quality of ESEF iXBRL filings from 4 countries, 2 where the ESMA ESEF mandate was made compulsory and 2 where it was voluntary.

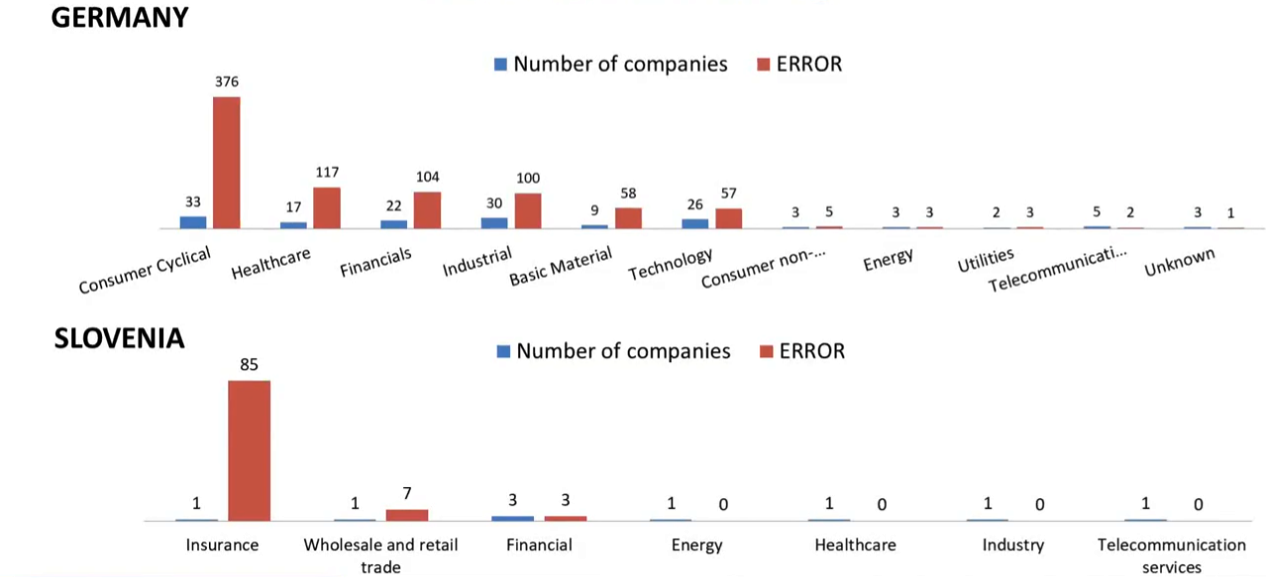

ESEF iXBRL filing errors by German and Slovenian companies (by industry)

As mentioned earlier, it was mandatory for companies in Germany and Slovenia to file their 2020 annual reports in the iXBRL format.

We surveyed 153 companies across 11 sectors in Germany and 9 companies across 7 sectors in Slovenia. The results from these countries are presented below.

The Consumer Cyclical sector in Germany was found to have the most errors (376) spread across 33 companies followed by the Healthcare (117 errors across 17 companies) and Financial (104 errors across 22 companies) sectors.

In Slovenia, an insurance firm was found to have 85 errors in its ESEF filing. This was followed by a firm in the Wholesale and Retail Trade sector with 7 errors in its ESEF iXBRL report.

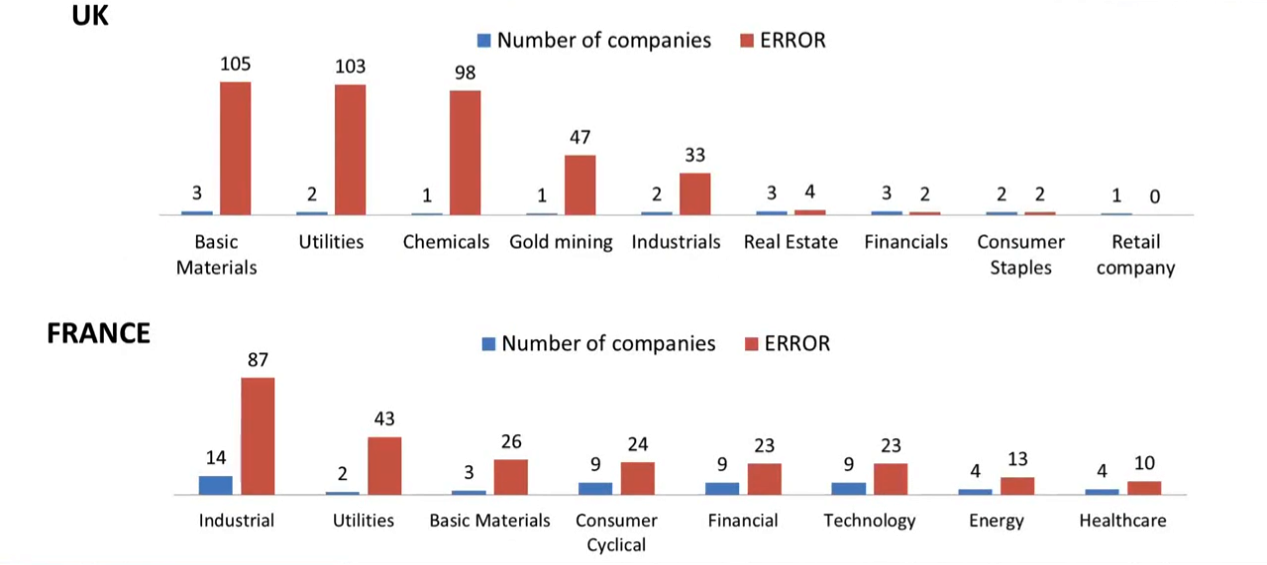

ESEF iXBRL filing errors by companies in the UK and France (by industry)

We surveyed 18 and 55 companies in the UK and France, respectively. Here’s what we found in assessing the quality of their ESEF iXBRL reports:

Companies from the Basic Materials sector in the UK had the most errors at 105, spread across 3 companies. This was followed by companies in the Utilities and Chemicals sector with 103 and 98 errors respectively.

In France, the situation wasn’t much different with the Utilities and Basic Materials sectors again featuring in the top 3 with 43 and 26 errors respectively. However, 14 companies in the Industrial sector accounted for 87 errors, making them top this list.

Conclusion

This article is meant to provide the reader with a birds-ey view of the ESEF filing landscape in the EU and the UK and how the quality of these reports has been. Since the mandate is new, it is natural to see many errors and warnings in the reports that have been submitted to the OAMs so far. However, we expect these to reduce substantially in the following years when companies become more comfortable with the regulatory reporting requirements laid down by ESMA.

In a subsequent feature, we will take a deep dive into what kinds of errors and warnings were found in the reports we surveyed and how companies can avoid these in the future.